Credit card debt in America has reached alarming heights, with recent statistics indicating that consumers owe over $1 trillion in credit card balances collectively.

Some reports show that approximately 41% of cardholders have been unable to pay off their balance in full each month, leading to an average debt of around $6,200 per individual. This surge in credit card debt can cause financial strain and anxiety for many, but it’s important to remember that there are effective strategies for using credit cards responsibly.

By understanding how to manage balances, make timely payments, and leverage rewards wisely, individuals can harness the benefits of credit cards while minimizing debt and enhancing their financial health.

Benefits of Using Credit Cards

You might be reading this thinking, “Why use credit cards in the first place?”

Using credit cards can offer several advantages that might help manage your finances and even provide some valuable perks in the process.

One of the most appealing benefits is earning rewards on purchases. Many credit cards offer rewards programs that allow users to accrue points, cash back, or travel miles based on their spending, which can lead to substantial savings over time.

For businesses, credit cards can help you organize finances by keeping personal and business expenses separate, making it easier to track spending and streamline your accounting. This separation is important for managing cash flow and keeping your accounting records straight.

Additionally, credit cards often come with various benefits that can provide perks and peace of mind. For example, travel protection offers coverage for trip cancellations, lost luggage, and travel accidents.

Some credit cards also include cell phone insurance that protects against damage or theft, while extended warranties can extend the manufacturer’s coverage on large purchases, providing added value and protection against unexpected costs. Overall, responsible use of credit cards can lead to enhanced financial flexibility and security.

1) Pay your balance off each month

To maintain control over your finances and avoid falling into the trap of high-interest debt, it’s absolutely essential to pay your credit card balance off in full each month is key. Otherwise, you’ll absolutely negate the benefits of using a credit card in the first place!

By doing so, you’ll save money on interest charges and improve your credit score, as a lower credit utilization ratio demonstrates responsible credit usage to lenders. Additionally, making timely payments helps you avoid late fees and potential negative impacts on your credit history.

Establishing a budget (aka spending plan) can help ensure you have the funds available to cover your monthly balance. Track your spending and set limits on how much you charge to your credit card, treating it like cash rather than an endless source of funds.

By being mindful of your spending habits and prioritizing paying off the balance, you’ll be better positioned to enjoy the benefits of credit cards without jeopardizing your financial stability.

2) Understand fees and interest rates

Before committing to a credit card, you have to research and understand common credit card fees, as they can affect your credit card experience and, eventually, your overall financial health.

Annual fees, for instance, are charged by some credit cards simply for the privilege of using the card, which may be worth it for those who can utilize the rewards effectively. Late fees can add up quickly if you miss a payment deadline, potentially exacerbating your debt situation and harming your credit score. Balance transfer fees can also come into play if you’re transferring existing debt to a new card for a lower interest rate, typically ranging from 3% to 5% of the transferred amount.

Above all, you must be mindful that interest rates can fluctuate based on various factors, including changes in creditworthiness, market conditions, or even the card issuer’s policies. Understanding how the Annual Percentage Rate (APR) may change, particularly if you miss a payment or exceed your credit limit, is vital to ensuring you don’t end up in a financial bind.

By being informed about these fees, you can understand how your spending habits will determine the total cost of using a credit card. From here, it’s time to choose the best card that works for you needs.

3) Compare credit cards

Now that you understand the potential fees and interest rates tied to your credit card, it’s time to compare card offerings and choose the one that most closely aligns with your spending habits and lifestyle.

For some, a card with an annual fee doesn’t make sense. However, the annual fee is very much justified for those who will use benefits like rewards and credits. For others who just need to separate personal and business expenses, a no-frills no-thrills business card with no-to-low rewards potential is sufficient.

If you’re looking to consolidate high-interest debt, a balance transfer card without rewards or perks may also work for you. For brand loyalists who like travel companies like:

A co-branded credit card could help you rack up rewards for travel and access elite status for even more perks like early check-in, more leg room, and more.

Don’t forget there are cards that will reward you for shopping for groceries, gas and other essentials. There are even great credit cards for foodies who like to eat or enjoy bespoke dining experiences and culinary events.

There are many cards to choose from, but the best one for your needs will determine which one you should get.

4) Stay organized

Nowadays, there are many ways to track your credit card usage. Budgeting apps like You Need a Budget (YNAB) or Every Dollar. I use Google Sheets with Google Calendar. It’s my preferred method of tracking my finances.

I also track my net worth (which keeps track of credit cards, too) with an app called Empower. For business expenses, I load transactions into Wave Apps accounting so I can categorize and reconcile bank statements. This tool is a lifesaver when it comes time to do income taxes!

Set apart time on your calendar weekly or biweekly to review your spending and

5) Improve your credit

If, for some reason, you can’t get the credit card you’re interested in or are having issues getting approved for premium credit cards, then it might be time to improve your credit score. Here are a few tips on getting started.

Pay down debt

To improve your credit score and gain access to better credit card offerings, it’s essential to focus on paying down any existing debt. High debt levels relative to your credit limit can negatively impact your credit utilization ratio, which makes up a significant portion of your credit score. Start by creating a debt repayment plan.

Create a budget, then separate funds to help you aggressively pay down debt. Consider strategies such as the avalanche method, where you prioritize paying off high-interest debt first, or the debt snowball method, which focuses on paying off smaller debts to gain momentum and encouragement.

Get Dave Ramsey’s Full Break-Down on the Debt Snowball Method here: The Debt Snowball Method Explained.

Monitor your credit

In addition to paying down debt, it’s crucial to monitor your credit report regularly. Doing so can ensure that all information is accurate and up-to-date. If there are any errors or discrepancies, you can dispute them with the credit bureau to potentially improve your score. You can also sign up for a credit monitoring service that will alert you of any changes or suspicious activity on your credit report.

Build a good credit history

Since this is an important factor in your credit score, it’s a good idea to focus on building a positive credit history. If you can’t get revolving credit accounts. Start with secured credit cards or credit builder loans with companies like Self or a company that adds positive rent payment history to to your credit profile. Pay your monthly bills on time, and you should see your credit history improve over time.

Get debt counseling

Debt counseling can offer valuable support for individuals struggling with overwhelming financial obligations, providing expert guidance on budgeting and repayment strategies. However, it may also come with drawbacks, such as potential service fees and the possibility of requiring participants to change their spending habits significantly. Ultimately, debt counseling can be a good first step toward financial recovery but should be considered alongside personal circumstances and goals.

Summing it all up

Credit cards can be valuable financial tools when used responsibly and wisely. It’s important to understand how they

Additionally, avoid accruing new debt during this process by sticking to your budgeting plan and avoiding unnecessary purchases. If you find it difficult to manage your payments, consider speaking with a financial advisor or credit counseling service, which can provide valuable guidance and tailored strategies to help you regain control over your finances. As you make consistent progress in paying down your debts, you’ll improve your credit score and increase your confidence in managing credit in the future.

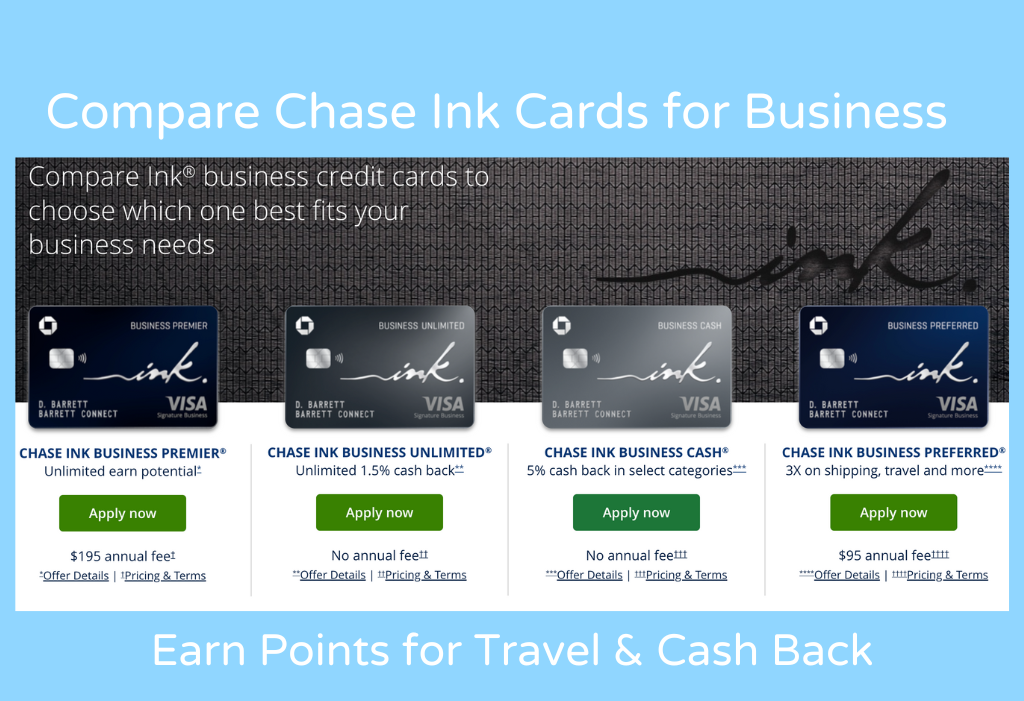

Are you ready to reap the benefits of RESPONSIBLE credit card usage? If so, check out these Chase Ink business credit cards that reward you for spending, come with loads of benefits and help you organize your business finances better.

Need help managing your finances? Explore these resources that can help you get out of debt quickly, too:

Need help managing your finances? Explore these resources that can help you get out of debt quickly, too:

Need help managing your finances? Explore these resources that can help you get out of debt quickly, too: